The high mortgage rates dashing your dreams of homeownership appear to be moving.

So whether buying a first home, splurging on a vacation getaway, or refinancing your current nest, keep an eye on what the Federal Reserve does next week.

Even though the Fed doesn’t control the nation’s mortgage rates, it does set them in motion.

So does the U.S. labor market, which frankly is hurting, if the latest jobs data are to be believed.

Here’s why these different parts of the economy impact the housing market and mortgage rates.

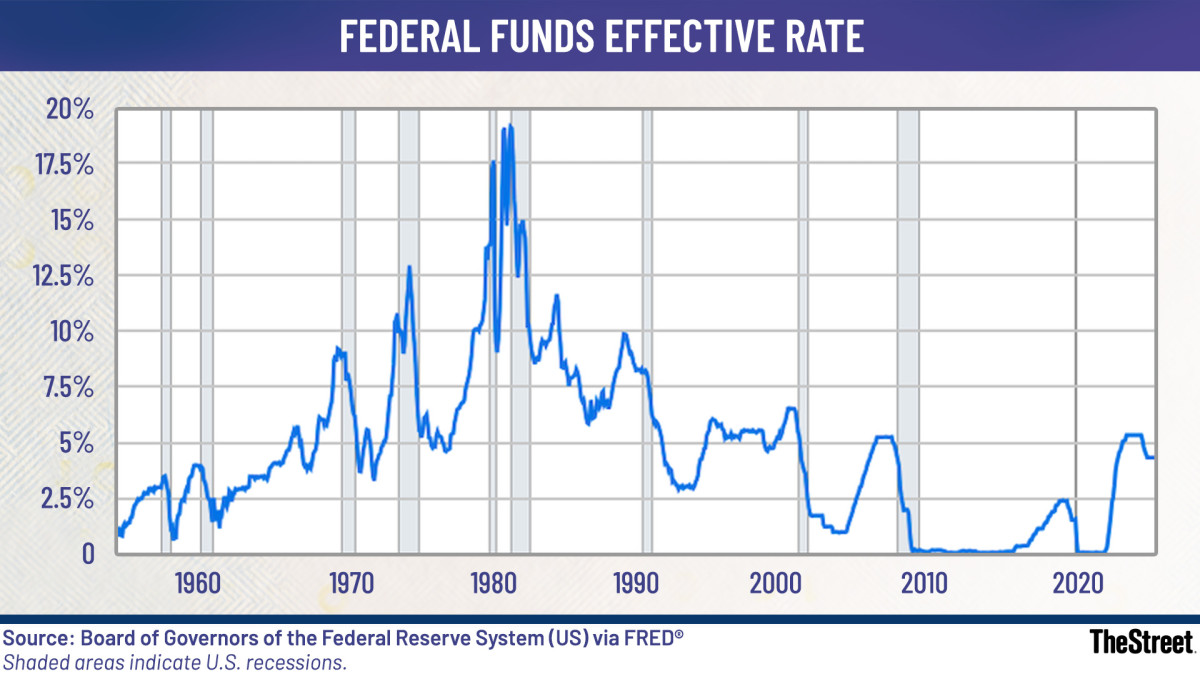

Source: Board of Governors of the Federal Reserve System

The Federal Reserve sets benchmark interest rates

- The Fed has a dual mandate from Congress to execute monetary policy that ensures maximum employment and price stability.

- The Fed has held the benchmark Federal Funds Rate steady since December 2024 at 4.25% to 4.50% in a “wait-and-see” approach for the impact of tariffs on inflation in the supply chain.

- Fed Chair Jerome Powell recently signaled an interest rate cut could be warranted in the near future amid a “shifting balance of risks.”

Weak jobs numbers spikes hopes for Fed rate cut

August job growth slowed down to a crawl, while the unemployment rate rose up to its highest level since the fall of 2021 during the Covid pandemic.

- The unemployment rate increased to 4.3%, as expected, from 4.2% in July, the Bureau of Labor Statistics reported Sept. 5.

- Nonfarm payroll jobs increased by only 22,000 in August, far below the estimate of 75,000.

- The revised June number showed a net loss of 13,000 jobs.

Treasury yields drive mortgage rates

In general, weaker jobs numbers prompt investors to buy bonds.

- Mortgage rates closely follow the yield on the 10-year Treasury note, which investors see as the safest long-term asset.

- Strong investor demand for Treasury bonds lowers the yields, which pushes mortgage rates down to make home loans cheaper.

- Rising inflation pressures Treasury yields higher, which translates into more expensive mortgages for homebuyers or owners looking to refinance.

What’s ahead at the Fed

The independent central bank will decide next week whether to cut interest rates to shore up the weakening jobs market and support economic growth or continue to hold rates steady to ward off higher-than-targeted inflation.

Market watchers say the weakening labor market all but clinches that the Federal Open Market Committee will cut the Federal Funds Rate by at least 0.25% on Sept. 17.

The CME Group FedWatch Tool shows an 89% chance of a 0.25% cut and an 11% chance of a 0.50% cut.

Some economists said a more dovish Fed could add 0.25% rate cuts in October and December, then another three in 2026.

More Federal Reserve:

- Fresh labor market data fuel Fed interest rate cut chatter

- Fed official sends bold 5-word message on September rate cuts

- New inflation report may have major impact on your wallet

- Morgan Stanley makes major change to Fed interest rate cut forecast

- Can the president fire a Federal Reserve governor?

Mortgage rates drop as jobs report plummets

“Investors are now increasingly confident that a 25-basis point cut is on the table [this] month, and some are even speculating that we could see a larger 50-point cut depending on upcoming economic data,” ONE Real Mortgage CEO Samir Dedhia told BankRate.

“This shift in sentiment is helping stabilize rates and boost borrower confidence,” Dedhia added.

Mortgage News Daily reported Sept. 6 that the average 30-year fixed rate mortgage rate fell to 6.29%.

This is the lowest since fall 2024.

“Mortgage rates haven’t come down significantly enough to bring back a flood of buyers,” Mariah O’Keefe, a Redfin agent, told Bloomberg.

Mortgage shoppers are “are on rate watch, hoping they’ll drop below 6%,” she added.

Related: Fed interest rate cuts hinge on looming inflation report

#Mortgage #rates #react #bets #rise #Fed #interest #rate #cut