We’re often told to get our affairs in order for our loved ones. Too often, though, some of our most loyal companions – our pets – are overlooked in estate planning. That doesn’t need to be the case.

With a pet trust, you can designate who will care for your furry (or feathered) friends and provide funds to cover their needs.

“When we think of pet trusts, we think of Leona Helmsley, who famously left $12 million for her Maltese, Trouble, in 2007,” said Colleen Carcone, director of wealth planning strategies at TIAA and author of “Principles of Estate Planning.

“While most people don’t have that kind of money, planning for pets is still a priority for animal lovers everywhere.” (A judge later reduced that trust to $2 million — still a powerful reminder that pets need formal planning.)

Source: TheStreet

Why pet trusts matter

A pet trust isn’t just about good intentions. It requires careful calculations based on your pet’s likely life span, the realistic costs of care, and your state’s legal requirements.

According to a J.P. Morgan Wealth Management report, a pet trust is a legal arrangement that sets aside funds for the care of your pets after your death or incapacity.

Longevity is a key factor. Veterinary research covering more than 15 million animals shows:

- Female dogs live about 12.8 years on average, males about 12.6 years.

- Cats live slightly longer, with females outliving males by almost a year.

- Smaller dogs outlive larger breeds; obese dogs live about 1.5 years less than healthy-weight dogs.

- Some species, such as cockatoos, can live 50-70 years, requiring decades of financial planning.

“These specifics matter when you’re calculating funding needs,” said Michelle Fait, a certified financial planner with Satori Financial in Seattle. “To start, multiply the annual cost of care by the expected number of years remaining in the pet’s life.”

Carcone said that in practice, people typically leave $5,000 to $10,000 per pet, though the amount can vary widely. Horses, for example, require much more because of boarding, food, and training costs.

How to set up a pet trust

Here’s what to include, according to J.P. Morgan and estate planning experts:

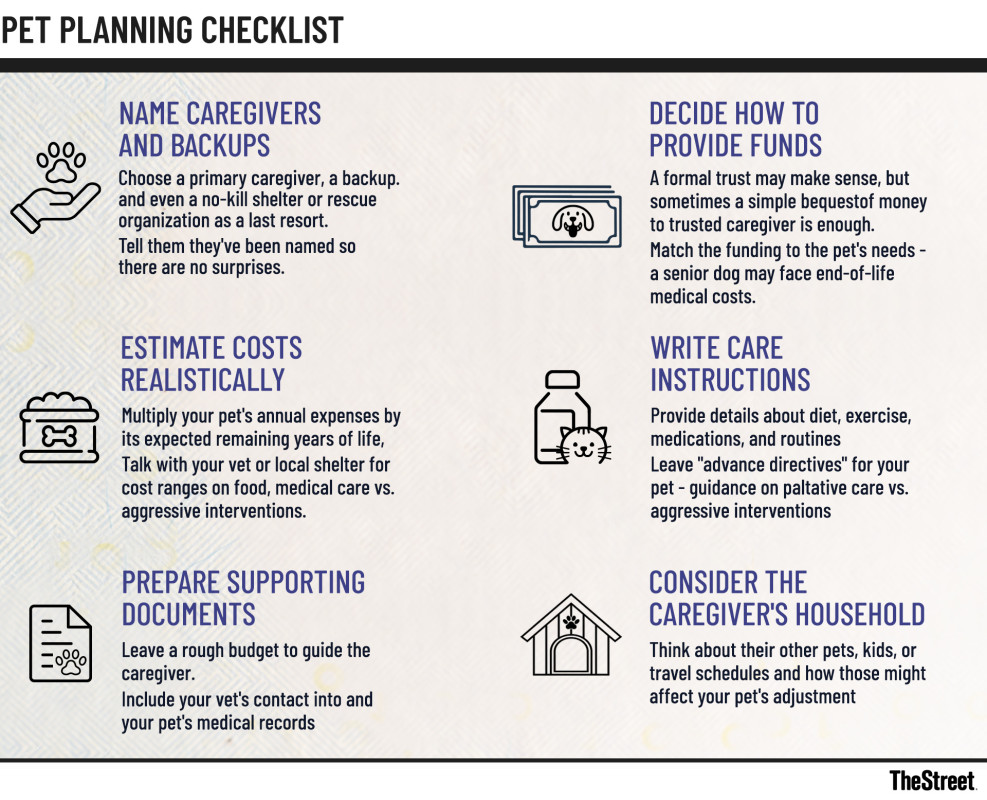

- Appoint a trustee to manage assets and ensure funds are used properly.

- Designate a caregiver to provide daily care — feeding, medical attention, companionship.

- Leave care instructions for diet, medical needs, exercise, and routines. Some owners even add end-of-life directives covering palliative care, major interventions, and final arrangements.

- Fund the trust realistically to cover food, veterinary care, grooming, sitters, and final disposition. Your veterinarian or local shelter can provide cost estimates.

- Outline an investment strategy for the funds.

- Specify duration and distribution — what happens to leftover funds once the pet dies.

“The two main decisions about care after a pet guardian’s death are: in whose care the pet will be left, and what resources will be left for their care,” Fait said. “Naming a primary caregiver, a backup, and even a successor organization like a no-kill shelter is key — and let the people know they’re named.”

Pet trust pitfalls to avoid

Even well-intentioned plans often fail for avoidable reasons.

- Not talking with caregivers: Always confirm your chosen person is willing and able to take on the task.

- Not naming alternates: Pets outlive plans; backups are essential.

- Forgetting practical details: Leave a budget, veterinary records, and your vet’s contact information. Consider how the caregiver’s household (kids, pets, travel) will affect your pet’s transition.

- Misunderstanding the law: “You cannot leave money directly to a pet,” Carcone stressed. “You can leave assets in trust to provide for a pet, but not to the pet itself.”

- Overlooking final distributions: Decide if leftover funds should go to the caregiver, a shelter, or another cause.

Fait also shared her personal experience to illustrate the costs: “I lost my dog this summer after 11 years together, and in addition to thousands of dollars in specialty vet costs, it was $600 for humane euthanasia. If the owner has pet insurance, make sure the caregiver knows about it and funds are left to continue paying premiums.”

Pet trust alternatives and next steps

Trusts are powerful but not always necessary.

“As for finances, you could use a trust, but it might be overcomplicating the situation,” Fait said. “If you trust the person with your beloved pet, you should be able to trust them with some money for their care.”

Carcone noted that leaving funds outright is simpler, but a trust provides more control. Trusts also come with administrative burdens: they require separate bank accounts, tax IDs, and sometimes income tax returns (Form 1041).

Either way, Carcone recommends working with an experienced estate planning attorney. “Remember, the funds typically will not be put in trust until after your death,” she said. “You won’t be here to fix problems if things aren’t set up correctly. Planning now ensures your beloved family members are cared for.”

The pet trust bottom line

Whether you set up a formal trust or leave money informally with a trusted caregiver, the key is advance planning. Pet trusts provide continuity of care, peace of mind, and a safeguard against uncertainty.

At the end of the day, this isn’t just about money. It’s about ensuring your companions receive the same thoughtful care as the rest of your family.

Related: White House makes risky changes to retirement accounts

#happen #pets #youre