Artificial intelligence holds the promise of revolutionizing industry, curing diseases, and solving humanity’s biggest problems.

It remains to be seen how it might do that with today’s large language models or AI-generated video, but in anticipation of the big boom, tech companies are spending billions to scale up their data centers and position for the coming revolution.

We’re not talking about a few billion, either. In recent weeks, eye-popping deals between AI giants have sent the markets to all-time highs. And finally, there’s been coming a concreteness to that spending and where it’s going.

Goldman Sachs

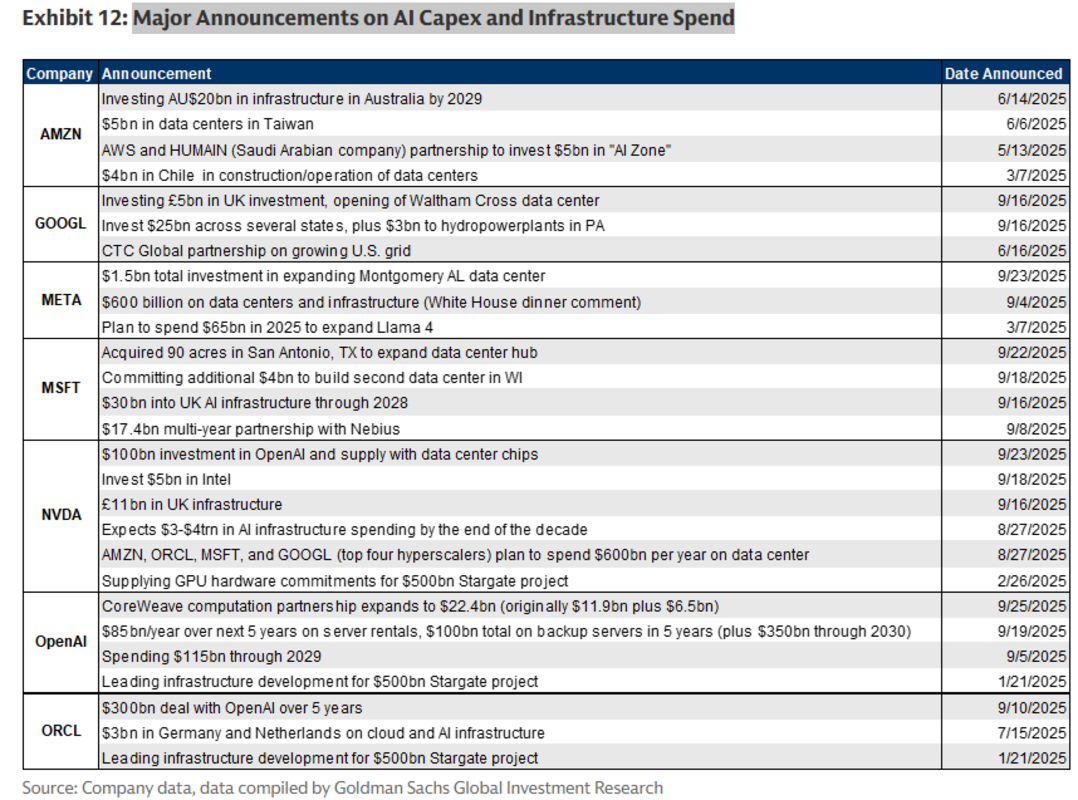

In August, chip giant Nvidia (NVDA) said that the top four hyperscalers would spend $600 billion per year on data center. Then, in quick succession, there was a $300 billion deal between hyperscaler Oracle and ChatGPT creator OpenAI.

Nvidia later announced a $5 billion investment in Intel (INTC) and a $100 billion investment in OpenAI, which comes with conditions to buy chips from the company. There’s also OpenAI agreeing to spend billions on chips with Advanced Micro Devices (AMD) , which comes with a warrant to acquire 10% of the company for a penny a share.

Related: Investors write off Oracle earnings miss as management promises stratospheric growth

This spending is already having an impact. Per Financial Times, 40% of U.S. GDP growth has come from AI investments. Some have called them a savior for the economy; maybe even more so for the markets, where they have represented 80% of returns.

However, the means by which firms are funding their big projects are garnering controversy and comparisons to the dot-com bubble. Specifically, the concentration with which these businesses are circulating money amongst themselves.

So is it cause for concern? Depends on who you ask.

Those Who Are Worried

With stock valuations starting to verge on ‘rich’ territory by many measures, some analysts are sounding the alarm on the arrangements.

Stephen Wu, the manager of hedge fund Carthage Capital and a former AI engineer at Amazon (AMZN) and Microsoft (MSFT) , considers himself concerned with the arrangement, saying that AI revenues increasingly look self-funded by the vendors versus end demand.

Wu cited Amazon’s $4 billion investment in Anthropic, which included commitments that the Claude creator would run on AWS and use their in-house chips. Google‘s (GOOGL) $2 billion follow-on investment in Anthropic, also came with a “multiyear deal worth more than $3 billion,” per WSJ.

Separately, there’s also the Nvidia investment in OpenAI which was made in recent weeks. There was also a separate deal between AMD and OpenAI, which came with a warrant to acquire 10% of the chipmaker for next to nothing. And on the data center fringes, an agreement between Nvidia and hyperscaler CoreWeave (CRWV) , which would see the chipmaker “purchase any unsold … cloud capacity through 2032.”

This mirrors the dot‑com boom, where companies used reciprocal transactions and vendor financing to inflate top lines. AOL Time Warner booked “round‑trip” ad deals to mask a slowdown. Qwest and Global Crossing swapped capacity to book revenue while burying costs as assets. When true demand fell short, the revenue evaporated and the write‑downs followed. Today’s AI financing webs are more sophisticated, but the economic rhyme is hard to ignore.

However, unlike 1999, today’s sponsors are cash‑rich incumbents with real businesses. That makes outright fraud less likely and gives time to learn into the spend. AI workloads appear real and growing. My take is that a bubble is forming but there are no signs of bubble bursting yet. Now that there is significant investment into AI, I’d watch for the follow-through. The real question now is will AI adoption rates and usage rates continue to grow at or faster than the rate we are expecting. Clearly, we are expecting this is a high rate, so even a medium-low rate might be a surprise to the downside.

However, the odd one out, Rich Privorotsky, Goldman Sach’s GS Head of European Delta One, actually argues that AI-exposed stocks still boast relatively reasonable valuations. The real concern ultimately comes down to Nvidia and OpenAI’s arrangements, or similar arrangements of vendor financing which became commonplace during the dot-com bubble:

“[I’m] definitely not old enough to have been around trading during the tech bubble and let’s level set, multiples are now where near that point in time. That said, vendor financing was a feature of that era and when when the telecom equipment makers (Cisco, Lucent, Nortel, etc.) extended loans, equity investments, or credit guarantees to their customers who then used the cash/credit to buy back the equipment… well suffice it to say, it did not end well for anyone.

Those Who Are Not (Sorta)

However, some are not so worried about the revenue roundtripping and incestuous relationships among firms… At least, not yet.

Perimeter Group Chief Investment Officer Todd Lemkin says that he’s not as worried about comparisons to the Dot-Com bubble, citing old-timey internet and telecom firms’ heavy reliance on debt for build-out. By contrast, many modern tech giants are giants unto themselves, with ‘country-sized’ valuations and scale.

“[These] businesses generate a lot of cash flow right now and may choose to take the excess cash flow and then go invest in things that don’t make money,” Lemkin said. “So I don’t think you’re going to see a loss of faith or a valuation crisis with the big players.”

Simply put, these firms are big and profitable already. They could simply stop spending on AI at any time and become more profitable.

That’s a viewpoint shared in part by LPL Research Chief Equity Strategy Jeff Buchbinder, who wrote that stocks are “definitely trading at elevated multiples” but they still remained reasonable when compared with the dot-com era.

LPL Financial

“The key difference between the broader secular AI growth theme and the dotcom era is that large, AI hyperscalers have mostly funded capital expenditures (capex) with strong internal cash flows, not through AI revneue in singularity or by issuing debt or equity,” Buchbinder says. “In comparison, dotcom era spending was broadly funded through massive amounts of ‘vendor financing’, which ultimately led to the circular flow of capital that fueled the bubble burst.”

Where’s the Problem?

Even more concerning, many of the companies shaking hands on these big deals have eaten up Americans’ retirement funds. The S&P 500 and Nasdaq 100 have converged, with the eight largest firms shared between the two indexes. Those firms represent 37.7% and 69.8% of the index; steep concentration by historical standards.

In retrospect, we might figure that just intuitively makes sense, especially if AI does start solving big problems. But we’ll need more time and data to make that evaluation for ourselves.

Too long, didn’t read? There might well be a bubble in the AI business; alternatively, valuations might just be getting ahead of themselves.

Where a Bubble Might Pop First

Regardless of where things land long-term, there’s a lot of evidence that somebody is inevitably going to lose in the short-run.

Lemkin says it will likely end up being real estate players and debt-encumbered hyperscalers like CoreWeave, which could become “collateral damage” of buy and lease agreements which have encumbered it with debt.

Shriram Bhashyam, COO of fund administration platform Sydecar, points out that the problems on the public equity size might me investment-related. “With a 3-to-4 year useful life of a chip or processor, and spending expected to multiply in the coming years, one has to squint to see the path to a return on investments.”

The situation might simply be more fraught in startups, where valuations are already steep and payoff is nowhere in sight. While publicly-traded firms have cash flow coming from strong core businesses, many early-stage businesses do not. Even OpenAI, an absolute goliath, is still losing billions per year.

#Deals #Starting #Weird #Analysts #Worried